W.A. Robinson: Important COVID-19 Announcements & Information READ MORE

Over the years, we’ve learned that one of the keys to our successful broker–underwriter partnerships is transparency. This means that we are open from the start about what we can offer and that brokers (like you) provide comprehensive information about their clients from the get-go.

This approach minimizes delays and rejections while maximizing successful outcomes for you and your clients.

With this in mind, let’s have an open discussion about the information that each of us require to create deals that work for everyone.

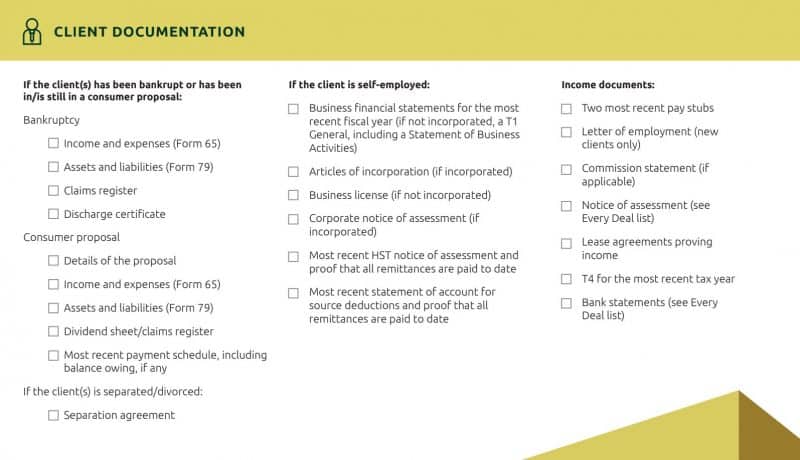

> Click on the visual to download Pillar’s Underwriting Checklist

Pillar is known for flexible, solutions-based mortgage lending, but there are some limits on what we can provide. When you understand the limitations of our underwriting process and mortgage offering, you can save yourself and your client time by recognizing which deals are a good match for Pillar – and which are not.

Two important constraints to remember:

7% is Pillar’s minimum mortgage rate

We pride ourselves on working creatively with brokers to come up mortgage terms that work for their clients – for example, by adjusting the amortization schedule to reduce monthly payments. However, we’re unable to offer rates below 7%, so we wouldn’t be the right fit for clients who are committed to finding a rate no higher than 5%.

80% is Pillar’s maximum Loan To Value (LTV)

While the big banks sometimes scale back their LTV for mortgages in rural areas, Pillar proudly offers up to 80% LTV for mortgages anywhere in Ontario. However, we can’t exceed this limit, so that means we’re unable to bundle fees into the deal on top of the 80%.

> Click on the visual to download Pillar’s Underwriting Checklist

When a deal is submitted to Pillar via Filogix, our underwriting team springs into action. Our ability to assess your client’s application and make our best offer in a timely manner depends on the supporting information that you provide. If delays occur, it is often because we have received an incomplete submission and need to pause the underwriting process while waiting for key documents.

Application components that are often overlooked in a submission:

Every deal is unique, so it’s critical that you provide the whole story for every application. The more information you can provide at the start of the process, the more quickly we can give you and your client the green light.

For a comprehensive list of the documentation that we require for different types of mortgage applications, please download the Pillar underwriting checklist.

copyright © 2024